: AI Innovation Warrants Higher Multiple")

Alphabet (NASDAQ:GOOGL) (NASDAQ:GOOG) the title performed well but was still not the most magnificent of so-called Magnificent Seven group over the past year. The artificial intelligence (AI) rally continues through 2024, and although Alphabet has big plans for AI innovation (perhaps better than some competitors), the stock still hasn’t not been able to generate much multiple expansion in recent years.

At the time of writing, GOOGL stock has a very reasonable forward price-to-earnings (P/E) ratio of 22.2 times, making it not only the “cheapest” Magnificent Seven stock, but also a name that is not too expensive than where the stock normally trades. The modest valuation alone leaves me incredibly bullish on the stock as the company looks to put its foot on the gas with Gemini (formerly Bard).

With Google recently pulling back the curtain on its paid Gemini Ultra tier, the company is essentially following in the footsteps of ChatGPT owner OpenAI. Hell, Gemini Ultra may seem to outperform ChatGPT-4 in some metrics. However, you can’t really call one or the other “best” for all uses, at least not yet.

Geminis are just as intriguing as they are capable. But is there something fundamentally wrong with the story of Alphabet, which remains at the forefront of AI innovation just like many of its peers?

There is a piece of hair in the GOOGL stock story. This lies in the high degree of uncertainty about the fate of Google Search once AI potentially becomes the go-to “internet guru.” For now, it’s unclear how many people will leave Google for greener pastures as new chatbots aim to capture a previously untouchable share of the search market.

AI is both a potential disruptor and a growth lever for Google

For now, it’s probably a known fact that Google relies heavily on the power of its search engine when it comes to sales and profits. Given Google’s heavy reliance on search, I guess you could say there’s a bearish scenario that would lead some to view the stock as a value trap.

Still, I think GOOGL avoiders and skeptics are wrong to view the name as a value trap simply because it’s the search heavyweight champion with everything to lose as consumer-facing AI becomes smarter and faster day by day.

On the contrary, generative AI products on Google could make the Google search experience even better. If there’s one company that can disrupt Google Search, it’s an AI chatbot built by Google.

Plus, Google chatbots are backed by one of the most enviable search engines (and datasets) on the planet. AI chatbot hallucinations (AI just makes things up) remain one of the biggest problems in AI today. As AI models – especially those created by Google – place more emphasis on citing sources (and the trustworthiness of said sources), we could see more links making good use of trusted websites with Google approval.

Knowing who and what to trust is vital, especially in the age of AI, where some users may simply believe their chatbots without verifying the source.

Could it be that a search-based LLM (large language model) is as good as the search engine behind it? Maybe. Only time will tell if research-based LLMs will become more popular than data-based ones that do not have access to the most up-to-date information. And with “edge AI” (on-device AI) on the horizon, it’s simply too early to tell how things will play out with AI models in the future.

Personally, I see the most use in a search-focused AI chatbot or a search engine that has a chatbot on the side, ready to help you on demand.

Alphabet’s ability to scale will be put to the test

Although Google Search is set to take a hit in the coming years, I am confident that Alphabet will be able to adapt as it seeks to diversify its revenue streams with a handful of powerful AI products. Just like Apple (NASDAQ:AAPL) was able to reinvent itself by moving from the iPod (the best-selling of the last generation) to the iPhone, Alphabet will be able to move from Google Search in the future as industry tides change.

Today, Search represents a considerable portion of the overall sales mix. But who knows what the breakup will look like in 10 years. I suspect that AI innovations will have evolved into services that diversify the company beyond research, perhaps putting it on a path to greater growth.

Autonomous vehicle services (think Waymo), AI-assisted drug discovery, doctor-friendly AI generative research, Google Cloud with AI, Gemini, and other intriguing technologies are essentially options that can contribute to the composition of income over time. Indeed, they could make Alphabet less of a search company and more of a disruptive AI company. That said, I consider Alphabet stock to be one of the cheapest AI stocks in today’s overheated, tech-driven market.

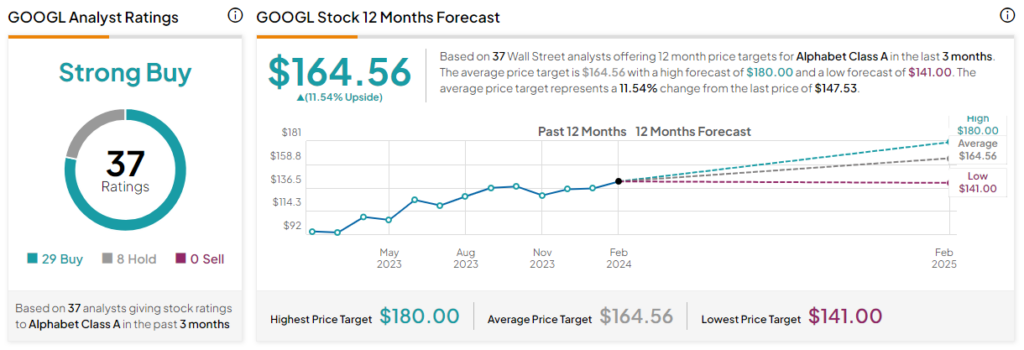

Is GOOGL Stock a Buy, According to Analysts?

On TipRanks, GOOGL stock is a Strong Buy. Out of 37 analyst ratings, there are 29 buy recommendations and eight hold recommendations. THE average price target for GOOGL stock is $164.56, implying an upside potential of 11.5%. Analyst price targets range from a low of $141.00 per share to a high of $180.00 per share.

Takeaways

Although GOOGL shares have been red hot, up almost 60% in the past year alone, he still seems lukewarm compared to some of his Magnificent Seven rivals. It remains to be seen whether Alphabet stock will heat up on AI to the magnitude of its peers. Either way, GOOGL stands out as a stock with GARP (growth at a reasonable price) written all over it. And it looks like a nice recovery, even though we’ve been waiting a long time for a market correction in the first half of the year.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.